After an accident settlement, one of the first practical questions is whether the IRS gets part of the money.

In many physical injury cases, settlement money that compensates you for the injury itself is not treated as taxable income. But a settlement may also include other categories of money, such as interest, punitive damages, lost wages, property damage, or emotional distress damages, and those categories may need separate tax review.

Are personal injury settlements taxable? You’ll learn that here.

Understanding the tax treatment of a settlement can help you plan ahead, keep better records, and know when to speak with a qualified tax professional. A personal injury lawyer can also help explain how the settlement describes the damages being paid.

This article is for general informational purposes only and should not be treated as tax advice. Tax treatment depends on the facts of your case, the wording of your settlement agreement, and current IRS rules. Speak with a qualified tax professional about your specific reporting obligations.

Are Personal Injury Settlements Taxable: Behind IRS Rules

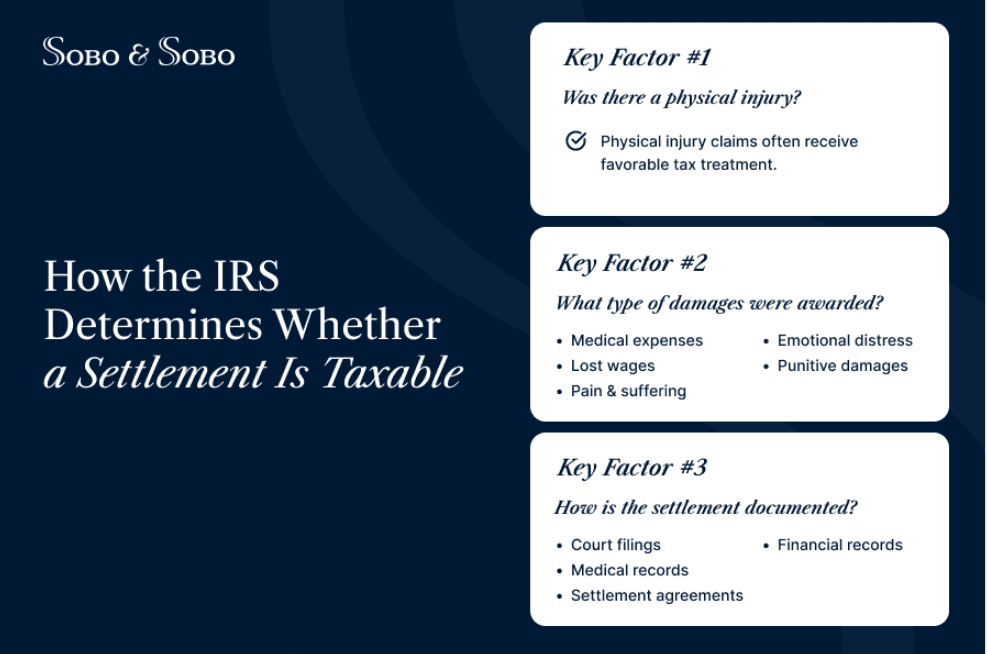

Under IRS rules, the tax treatment of settlement money usually starts with the nature of the claim. The key question is not simply how much money was paid, but what the payment was meant to compensate.

Settlement documents, medical records, court filings, and payment records may all help show what the money was meant to cover.

Caption: The IRS looks at the nature of the claim, damages awarded, and settlement documentation.

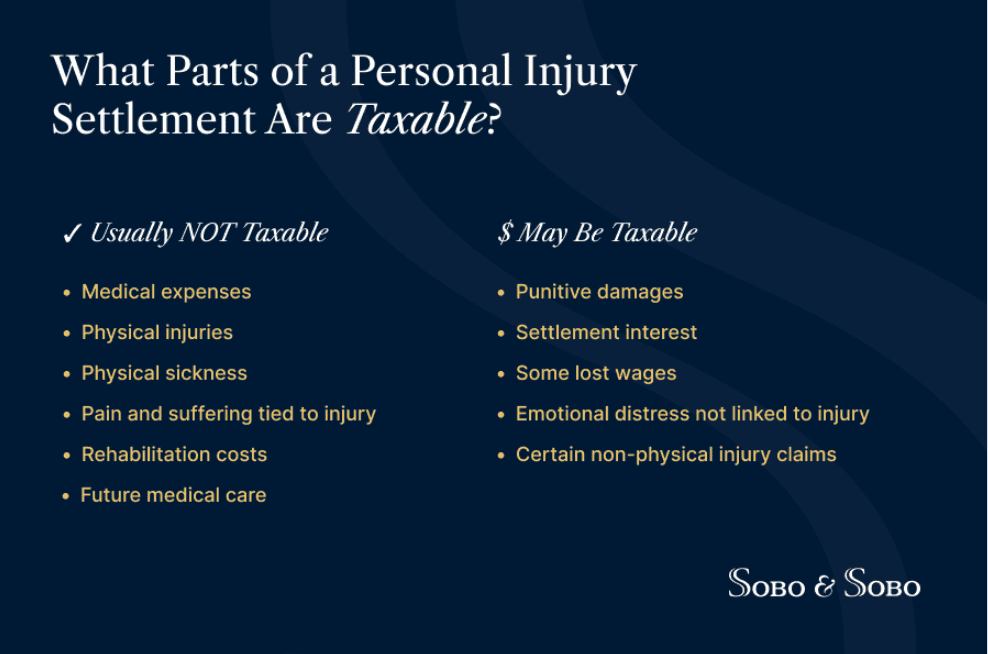

Which Parts of a Settlement May Be Taxable?

The tax question often comes down to allocation. A single settlement check may represent several different categories of damages, and each category may be treated differently.

Physical Injury Compensation

This category usually includes medical treatment, rehabilitation, future care, and pain and suffering connected to the injury. The settlement agreement should make that connection clear.

Lost Wages and Taxable Income

Lost wage damages can be more complicated because they may replace income that would otherwise have been taxed. The tax treatment can depend on the underlying claim and how the settlement agreement allocates the payment.

Emotional Distress Damages

Emotional distress damages are one of the areas where the details matter most. The key question is whether the distress is connected to a physical injury or stands on its own as a separate, non-physical harm.

Punitive Damages and Taxation

Punitive damages are generally taxable because they are meant to punish wrongdoing, not compensate the injured person for medical care or physical harm.

Interest on Settlements

Interest is usually treated separately from the injury compensation itself. Even when the underlying injury payment is not taxable, interest added before or after judgment may be taxable income.

Speak with Sobo & Sobo to learn how different types of damages may affect your compensation.

Are Car Accident Settlements Taxable?

Car accident settlements often include more than one type of payment. The agreement may account for medical care, pain and suffering, vehicle damage, lost wages, or interest. Those categories should not be lumped together when reviewing possible tax issues.

Medical Expenses After a Car Accident

Medical reimbursement is usually easiest to understand when the payment is tied directly to accident-related care, such as emergency treatment, hospital stays, physical therapy, medication, or follow-up visits.

Property Damage Claims

Property damage is separate from injury compensation. The tax consequences may depend on the value of the property, repair costs, and whether the payment exceeds the property’s adjusted value.

If your car accident settlement includes several categories of damages, Sobo & Sobo can help you understand which portions may need tax review.

Learn more: What to do after a car accident?

Do You Pay Taxes on Pain and Suffering?

Pain and suffering is often one of the most confusing parts of a settlement because the tax treatment depends on what caused the suffering.

When Pain and Suffering Compensation Is Tax Free?

Pain and suffering is usually reviewed by looking at what caused it. Pain caused by broken bones, surgery, or another documented accident injury is usually treated differently from distress that is not tied to physical harm.

Situations Where Damages May Become Taxable

Taxation may apply when damages are tied to non-physical injuries, certain employment claims, or emotional distress that is not connected to a physical injury.

Caption: The tax treatment of a settlement depends on the type of damages awarded

Why Some Lawsuit Settlements Are Taxed Differently?

Not all lawsuit settlements receive the same tax treatment.

The IRS looks at what the lawsuit was about. A settlement for unpaid wages, business losses, discrimination claims, or contract disputes may be treated differently from compensation tied to an accident injury.

The same dollar amount can receive different tax treatment depending on whether it compensates physical injury, lost income, business harm, emotional distress, interest, or punitive damages.

Learn more on how the personal injury process actually works.

How the IRS Determines Whether a Settlement Is Taxable?

Are personal injury settlements taxable in your case? Here’s how the IRS decides.

Tax authorities generally look beyond the total settlement amount. The key question is what the money was meant to replace or compensate.

Settlement Wording and Documentation

Settlement documents matter because they may identify how the payment is divided among different categories of damages. The wording can help a tax professional understand what was paid and why.

Important records may include the settlement agreement, medical records, court filings, payment documents, and tax-related correspondence.

How Legal Guidance Can Help Before and After Settlement

A personal injury lawyer can help review the legal terms of a settlement before the agreement is finalized. That review may include whether the agreement identifies the damages being paid, whether important records are preserved, and whether a tax professional should also review the payment.

Reviewing Settlement Terms

Clear settlement language can reduce confusion later if questions arise about what the payment covered.

Coordinating With a Tax Professional

A lawyer can explain the legal claim and settlement terms. A qualified tax professional can advise on reporting obligations.

Concerned about protecting your settlement? Contact Sobo & Sobo for a free consultation.

What to Do After Receiving Your Settlement?

Once settlement money is paid, keep the paperwork. Save the settlement agreement, medical records, payment documentation, tax forms, and correspondence explaining what the settlement covers.

These records can help a tax professional understand what was paid and why.

If you are unsure whether part of your settlement is taxable, speak with a qualified tax professional.

Discover what a personal injury lawyer is and what they do for injury victims.

Frequently Asked Questions

Are personal injury settlements taxable?

Generally, compensation for physical injuries or physical sickness is not taxable. Punitive damages, interest, and some damages unrelated to physical injury may be taxable.

Are car accident personal injury settlements taxable?

Car accident settlement money tied to physical injuries is generally not taxable under federal law. Other parts of the settlement may need separate review.

Is pain and suffering taxable?

Pain and suffering is generally not taxable when it results from physical injuries or physical sickness. If it is not tied to physical harm, the tax treatment may be different.

Do you have to pay taxes on a lawsuit settlement?

It depends on what the lawsuit was about and what the payment is meant to compensate. Injury settlements, employment settlements, business disputes, punitive damages, and interest can receive different tax treatment.

What part of a personal injury settlement is taxable?

Punitive damages, interest, and some non-physical injury damages are among the portions that may be taxable.

Are emotional distress damages taxable?

Sometimes. Tax treatment often depends on whether the emotional distress is tied to a physical injury.

Can the IRS take part of my settlement?

If part of your settlement is taxable, you may owe taxes on that portion. A qualified tax professional can help determine what must be reported.

Still Wondering if Personal Injury Settlements Are Taxable?

Settlement tax questions can be confusing when one payment includes several categories of damages, such as medical costs, lost wages, emotional distress, interest, or punitive damages. Sobo & Sobo can help you review the legal terms of your injury settlement and identify questions to discuss with a qualified tax professional.

Contact Sobo & Sobo today for a free consultation.